Utah Banks Are Quietly Rewriting the Rules on Fintech Risk

Utah banks and a leading fintech attorney reveal how sponsor banking and BaaS partnerships have shifted: stricter oversight, higher operational standards, and relationship-driven frameworks are raising the bar for fintechs—and expanding access to modern financial services.

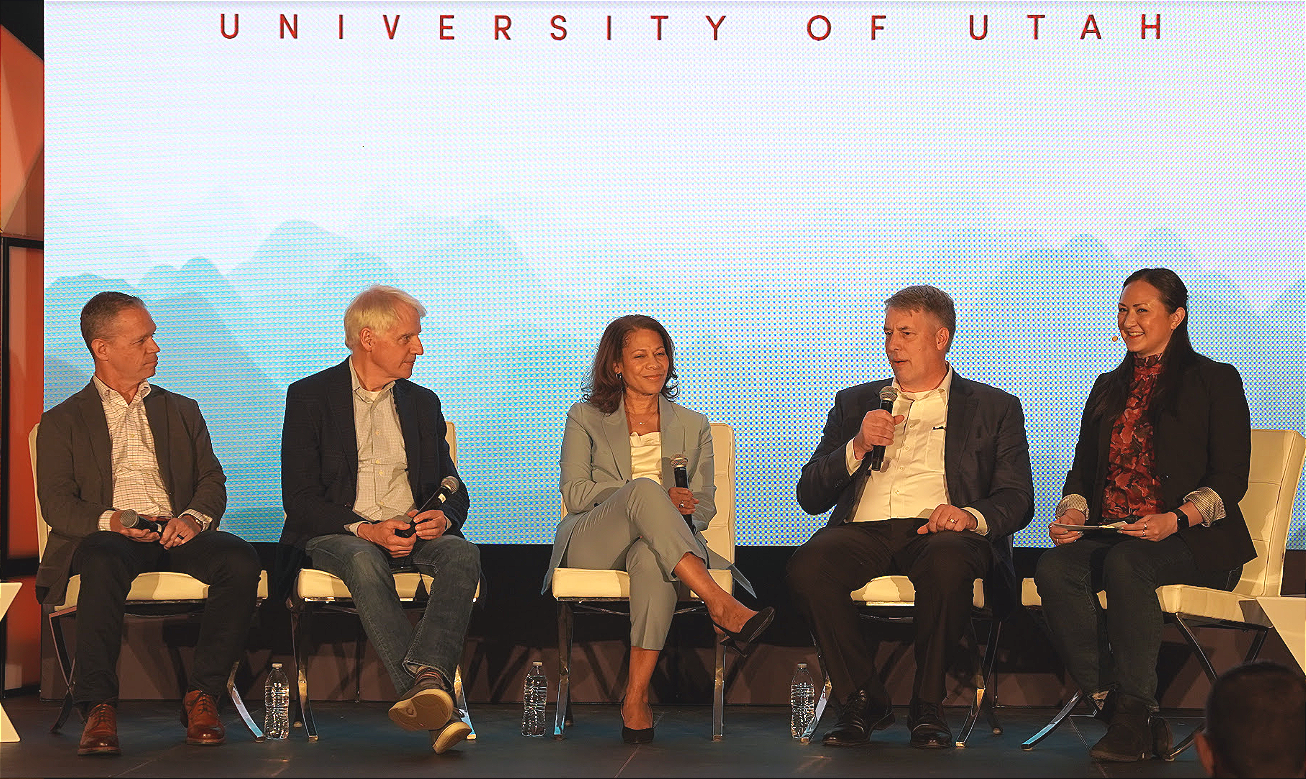

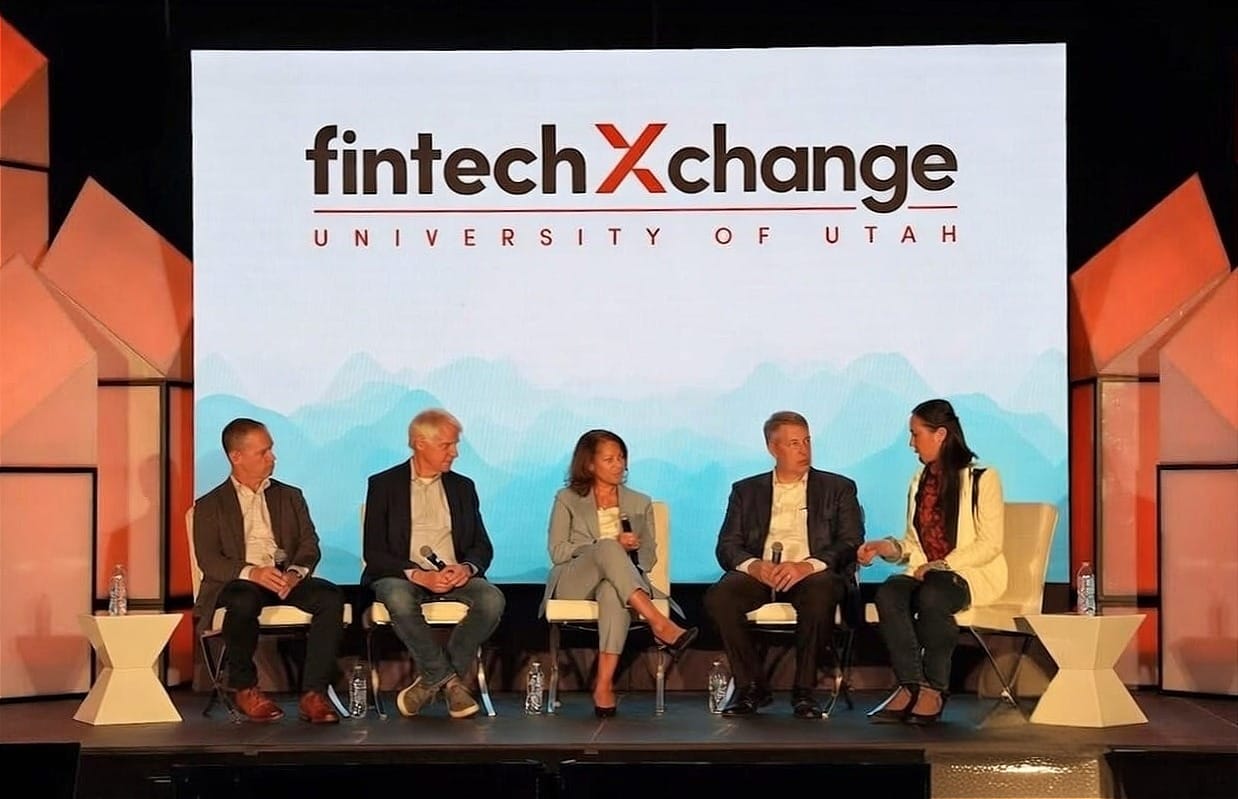

Brian Jones (President, Merrick Bank); Kent Landvatter (CEO & Executive Chairman, FinWise Bank); Obrea Poindexter (Partner, Cooley LLP); Brian Enneking (COO, First Electronic Bank); and moderator Kiah Lau Haslett (Creator, Fintech Takes Banking, Workweek) at the Fintech Xchange panel on sponsor banking and BaaS, February 5, 2026, Salt Lake Hilton

Brian Jones (President, Merrick Bank); Kent Landvatter (CEO & Executive Chairman, FinWise Bank); Obrea Poindexter (Partner, Cooley LLP); Brian Enneking (COO, First Electronic Bank); and moderator Kiah Lau Haslett (Creator, Fintech Takes Banking, Workweek) at the Fintech Xchange panel on sponsor banking and BaaS, February 5, 2026, Salt Lake Hilton

Salt Lake City, Utah – February 5, 2026

At a Fintech Xchange panel on sponsor banking and BaaS, Utah banks and a leading fintech lawyer delivered a blunt reality check: the bank–fintech–regulator relationship has fundamentally shifted, and the stakes are higher than ever.

Moderated by Kiah Lau Haslett (Workweek, Fintech Takes), the session —Building Sustainable Partnerships in the New Era of BaaS —featured:

Brian Jones, President, Merrick Bank (South Jordan, UT)

Kent Landvatter, CEO & Executive Chairman, FinWise Bank. (Murray, UT)

Obrea Poindexter, Partner, Cooley LLP, a Palo Alto–headquartered international law firm specializing in corporate, regulatory, and technology law, with deep experience advising fintech and financial services clients.

Brian Enneking, COO, First Electronic Bank (Salt Lake City, UT)

What might have sounded like a lecture on exams, consent orders, and data schemas actually revealed the practical truths for founders, investors, and operators: compliance and sophistication are now table stakes, and shortcuts aren’t tolerated.

Brian Jones (President, Merrick Bank); Kent Landvatter (CEO & Executive Chairman, FinWise Bank); Obrea Poindexter (Partner, Cooley LLP); Brian Enneking (COO, First Electronic Bank); and moderator Kiah Lau Haslett (Creator, Fintech Takes Banking, Workweek) at Fintech Xchange panel Building Sustainable Partnerships in the New Era of BaaS, February 5, 2026, Salt Lake Hilton

Regulators Aren’t Sleeping—They’re Data-Diving

Enneking framed the new reality bluntly: these sponsor banks touch “30 or 40 million consumers a year. We operate with the same impact as a bank many times our size, and regulators are going to hold you to that. They’re going to hold you to the same level of expectations.”

Exams aren’t getting lighter—they’ve become longer, deeper, and entirely data-driven. Enneking explained that regulators now expect banks to “know the answers before we even have to go talk to our fintech partners.” Analysts can’t treat fintech partners as black boxes anymore; they must have a clear line of sight into every product, every partner, and every transaction.

The panel also acknowledged that regulators have made remarkable progress in catching up with the pace of fintech innovation. Yet, as Landvatter warned, “If you’re applying rules that were written prior to these innovations, you risk rolling back the clock and excluding people from banking services.” Even as regulators modernize, legacy frameworks still apply in ways that can misfire.

This Isn’t a Vendor Contract—It’s a Partnership

Poindexter drilled home a central theme:

“These are not vendor relationships. One size fits all doesn’t work for bank–fintech relationships. There needs to be a clearer mindset that this is a relationship, not a vendor. Just like any relationship, there needs to be flexibility. Banks and fintechs share risk, compliance responsibilities, and reputations, and the regulatory guidance should recognize that.”

Salt Lake City Hilton hosted the 4th annual Fintech Xchange, featuring a panel with Brian Jones (President, Merrick Bank); Kent Landvatter (CEO & Executive Chairman, FinWise Bank); Obrea Poindexter (Partner, Cooley LLP); Brian Enneking (COO, First Electronic Bank); and moderator Kiah Lau Haslett (Creator, Fintech Takes Banking, Workweek); February 5, 2026

In practice, this means banks and fintechs must treat each other like strategic partners, not software providers. Poindexter added:

“There should be a different framework developed for bank–fintech relationships, with guidance really focused on those types of partnerships and their specific offerings.”

Consent Orders Didn’t Crush the Industry. They Educated It.

A wave of consent orders slapped many BaaS players awake. Enneking said the experience forced self-reflection:

“We just became very self-reflective on what we were doing well and what we weren’t, and how we could get better. One of the things we focused on was really improving our access to data from all of our financial products… That started to transform the way that we monitor.”

Brian Jones (President, Merrick Bank); Kent Landvatter (CEO & Executive Chairman, FinWise Bank); Obrea Poindexter (Partner, Cooley LLP); Brian Enneking (COO, First Electronic Bank); and moderator Kiah Lau Haslett (Creator, Fintech Takes Banking, Workweek) at Fintech Xchange panel Building Sustainable Partnerships in the New Era of BaaS, February 5, 2026, Salt Lake Hilton

Landvatter noted that some banks “got into this thinking it was going to be very easy—and scaled maybe too fast—leaving a legacy that we’re all trying to live with. At the same time, it set the bar higher. Prior to that, fintechs were asking, ‘How fast can I get to market and how many regulations do I have to follow?’ It’s 180 degrees different now, which I think is so healthy.”

Poindexter emphasized the fintech-side shift: consent orders forced alignment and regulatory understanding. “They helped educate parties—especially non-banks—about the framework their banks had to comply with, and therefore what they, as partners, needed to meet. It’s been a wake-up call for the whole ecosystem.”

Financial Inclusion Matters

Landvatter tied these changes to a broader mission: expanding access.

Kent Landvatter (CEO & Executive Chairman, FinWise Bank) and Obrea Poindexter (Partner, Cooley LLP); at the Fintech Xchange panel on sponsor banking and BaaS, February 5, 2026, Salt Lake Hilton

“The fintech aspect of partnering with banks is about delivering banking products where people need them, to a broader audience, and in a way that’s unique to them. If you apply old rules blindly, you risk rolling back access to people who really need innovative financial services.”

Bank–fintech partnerships, when done thoughtfully, aren’t just about revenue—they’re about inclusion.

Tech Grind: Normalize or Perish

Behind regulatory and strategic conversations lies the unsung grind: tech stacks. Every fintech partner has its own loan origination system, data model, and product flow.

“All that data is defined completely differently. It’s all named different things… Our approach is to create a schema that normalizes that data. Otherwise your analysts have to become an expert in the tech stack of every one of your partners, and that just does not scale,” said Enneking.

FinWise took a proactive approach:

“We wanted to capture all the data. We wanted to API directly into the fintech… It was a fun discussion with the board. I said, ‘We’ve got to build New York City before the first person moves in.’”

Kiah Lau Haslett (on right, Creator, Fintech Takes Banking, Workweek), moderating a panel Building Sustainable Partnerships in the New Era of BaaS that included Brian Jones (President, Merrick Bank); Kent Landvatter (CEO & Executive Chairman, FinWise Bank); Obrea Poindexter (Partner, Cooley LLP); and Brian Enneking (COO, First Electronic Bank); February 5, 2026, Salt Lake Hilton

Early-Stage FinTechs: Grow Up or Get Left Behind

Poindexter didn’t sugarcoat the reality for startups:

“It literally breaks my heart when early-stage fintechs I’ve been working with are getting dropped by one bank, then they go to another bank and can’t create a relationship.”

Landvatter explained the new bar for entry:

“Prove your business model through a state licensing approach… If you can prove that, then when we take a look at a fintech, we run it through third-party oversight, but we also look at it somewhat like a VC. We’d never take one that just got $500,000 from an inheritance and started, even if it’s a really neat idea. Go prove it in a licensed form and try to build that a little more organically.”

Compliance and operational maturity are now table stakes for anyone hoping to partner with a sponsor bank.

Risk Appetite and the Long Game

Banks must decide how much control they retain versus how much they trust partners. Jones summarized Merrick’s approach:

“Sometimes we take on risks that other bankers might be uncomfortable with, and we’ve managed them successfully for a long period of time. Different risk, but one we think we can make money at and do in a safe and sound way.”

Landvatter echoed the family analogy for BaaS risk:

“Just going into the BaaS banking system is seen by some as extremely risky. But once you’re in the space, there’s a way to manage it to a level that you feel comfortable with.”

Poindexter’s parting line was both human and practical:

“It’s like any relationship you have with your spouse or your children. It takes work—a lot of work—and communication.”

The Salt Lake City Hilton Grand Ballroom was the location for the 4th annual Fintech Xchange panel with Brian Jones, Kent Landvatter, Obrea Poindexter, Brian Enneking, and moderator Kiah Lau Haslett, February 5, 2026

Bank–fintech partnerships are no longer just a revenue play—they’re high-stakes, relationship-driven ecosystems. Success requires discipline, operational maturity, and constant communication. For Utah’s founders, investors, and executives, the message is clear: treat these alliances like long-term partnerships, not vendor contracts, and build systems and compliance frameworks that can withstand both regulatory scrutiny and rapid innovation. The banks that embrace this rigor—and the fintechs that align—will define the next generation of accessible, scalable, and responsible financial services. In sponsor banking, shortcuts don’t pay. Only strategic trust and high-discipline execution do.