Utah Leaders and SEC Commissioner Hester Peirce Tackle the State's IPO Gap

SEC Commissioner Hester Peirce joined a Dorsey & Whitney roundtable in Salt Lake City to discuss regulatory reforms aimed at making IPOs more accessible, as Utah business and policy leaders examined how to grow the state's pipeline of public companies.

Troy Keller, Partner at Dorsey & Whitney LLP, moderating a discussion about IPOs with Hester Peirce, Commissioner, United States Securities and Exchange Commission (on screen) and a room full of Utah business, legal, financial and policy leaders, Dorsey & Whitney's Salt Lake City offices, June 8, 2026

Troy Keller, Partner at Dorsey & Whitney LLP, moderating a discussion about IPOs with Hester Peirce, Commissioner, United States Securities and Exchange Commission (on screen) and a room full of Utah business, legal, financial and policy leaders, Dorsey & Whitney's Salt Lake City offices, June 8, 2026

A candid roundtable at Dorsey & Whitney put Utah's public-offering future on the table — and brought a key SEC voice into the room.

Salt Lake City, Utah — June 8, 2026

Yesterday in downtown Salt Lake City, roughly three dozen leaders from Utah's business, legal, financial, and policy communities gathered at the offices of Dorsey & Whitney for a conversation that has been a long time coming: how do we get more Utah companies to go public?

The roundtable, co-hosted by Dorsey & Whitney and TechBuzz News, drew capital markets attorneys, investment bankers, trade association executives, state agency officials, biotech accelerator leaders, fintech CFOs, and, notably, Hester Peirce, who serves as a Commissioner on the United States Securities and Exchange Commission, who joined virtually from Washington.

Hester Maria Peirce, Commissioner, United States Securities and Exchange Commission

The stated agenda centered on two questions: Is it important for more Utah companies to pursue IPOs? And if so, what, realistically, can be done to make that path more viable?

The answer to the first question was never seriously in doubt. The second occupied the better part of two hours.

Why It Matters: Headquarters, Wealth, and the Micron Lesson

Troy Keller, a partner in Dorsey's capital markets group and one of the roundtable's organizers, framed the stakes early. The number of U.S. public companies has fallen by roughly half since its peak in the mid-1990s — from around 8,000 to closer to 4,000 today — as private capital has grown more accessible and regulatory burdens have made public markets less attractive. The consequences, he argued, are not abstract.

Troy Keller, Partner, Dorsey & Whitney LLP

"When a company goes public, the headquarters stays in the state," Keller said. "If the exit is acquisition or private equity roll-up, the decision makers are no longer here in all likelihood."

The academic evidence backs him up. Research by Butler, Fauver, and Spyridopoulos found that each $10 million in IPO proceeds generates roughly 41 local jobs, plus about 0.7 new local businesses and measurable gains in spending, real estate, and in-migration. A 2024 study by Babina, Ouimet, and Zarutskie tied 8.2% of missing startup employment directly to the IPO decline, finding that going public sends employees out to found new ventures. Local patent filings also rise following a hometown listing, most sharply where the newly public company is a significant share of a smaller local economy.

He reached back to his Idaho upbringing for the sharpest illustration: Micron Technology, the Boise-based semiconductor firm that went public in 1984, joined the trillion-dollar market cap club on May 26, 2026 — only the third U.S. chipmaker ever to reach that threshold — and recently announced an expansion that will add an estimated 17,000 Idaho jobs on top of the roughly 7,000 already there. "Does that happen if Micron doesn't go public? Absolutely not."

Closer to home, Keller pointed to four Utah anchors. Zions Bank has been public since 1966, now carries roughly $89 billion in assets, and employs about 10,000 people across the West. Nature's Sunshine, public since 1978, pioneered Utah's natural-products and direct-selling model, a cluster that by 2020 anchored more than 38,000 Utah jobs and over 70% of the state's non-gold exports. Novell, which went public in 1985 and ran much of the world's networks at its peak with some 10,000 employees, seeded a generation of Utah County founders. And Qualtrics, whose 2021 IPO at roughly $1.55 billion remains the largest tech IPO in Utah history, now has alumni seeding a new wave of Silicon Slopes startups.

Shawn Lindquist, joining virtually, has seen the dynamic play out firsthand. Lindquist is a seasoned Chief Legal Officer with nearly 30 years of experience guiding high-growth technology companies through IPOs, major financings, strategic transactions, and complex regulatory environments. A key figure in Utah’s Silicon Slopes ecosystem, he is widely recognized for helping lead four Utah-linked companies through successful IPOs or public listings, providing deep firsthand insight into the local economic and entrepreneurial ripple effects of going public.

Among the attendees who could speak to the experience most recently was Sanchaita "Sanch" Datta, President and Co-founder of Salt Lake City-based Fat Pipe Inc., which completed a Utah IPO in 2025. "It was something we had wanted to do for a long time, and it was a successful IPO," Datta said. Fat Pipe's offering was modest — raising under $5 million — but it demonstrated that the path remains open even for smaller companies willing to pursue it.

Jonathan Leus, Managing Director and Head of Securities Underwriting at Zions Capital Markets.

Jonathan Leus, Managing Director and Head of Securities Underwriting, Zions Capital Markets, argued that companies are remaining private far longer than they did in previous decades, concentrating much of their value creation among private investors. He noted that Amazon and Microsoft went public with market capitalizations of only a few hundred million dollars, allowing retail investors to participate in decades of subsequent growth. By contrast, SpaceX is expected to debut at a valuation of roughly $1.7 trillion. "The retail side of the business had a chance to ride that upswing in valuation from the 80s and 90s," Leus said, adding that wealth creation is increasingly concentrated on the institutional side of the market.

The Cost and Complexity Problem

Before Commissioner Peirce joined the call, participants worked through the practical barriers that keep companies from pursuing an IPO even when the strategic logic might favor one.

Erika Whitmore, Salt Lake City Office Managing Partner, KPMG, speaking to the attendees at the Dorsey Whitney - TechBuzz IPO Roundtable

Erika Whitmore, KPMG's Salt Lake City Office Managing Partner and a veteran of more than a dozen mountain-region IPOs, walked through the process in detail. The planning phase alone, from the decision to go public through the organizational kickoff, runs six to eighteen months. The formal IPO process then takes another four to six months: confidential S-1 filing, an initial SEC review of roughly thirty days, comment letter exchanges, public filing, road show, and pricing. Accounting costs, she said, typically run from 0.11% to 0.50% of total annual revenue for a revenue-generating company — under 1% — or up to 1.25% of gross proceeds, depending on the company's risk profile, audit history, offering size, and number of comment-letter rounds. The most common SEC comment areas, per KPMG's experience, are MD&A disclosures, non-GAAP measures, segment reporting, revenue recognition, and internal controls.

David Marx, Partner, Dorsey Whitney's Corporate Group and Co-Chair, Capital Markets Practice Group, speaking to the attendees at the Dorsey Whitney - TechBuzz IPO Roundtable

David Marx, Partner, Dorsey Whitney's Corporate Group and Co-Chair, Capital Markets Practice Group, put legal costs in a range of $500,000 to $2 million. "It depends on the factors," he said, noting that expected SEC regulatory changes should bring those numbers down significantly.

Whitmore was cautiously optimistic. She noted that several startup companies she's currently working with in Utah are running accounting departments roughly half to a third the size of comparable companies just two years ago, largely due to AI-assisted workflows. "I think it could explode," she said.

Erika Whitmore, KPMG's Salt Lake City Office Managing Partner, speaking to the attendees at Dorsey's Salt Lake office conference room, Dorsey Whitney - TechBuzz IPO Roundtable, with David Jensen, Tax Partner, KPMG

Analyst coverage surfaced repeatedly as a structural problem specific to smaller issuers. Rich Ludlow, senior corporate counsel at Varex Imaging Corporation, a Salt Lake City-based, NASDAQ-listed X-ray imaging equipment manufacturer and Utah's self-described "best kept secret," put it plainly: more coverage means more exposure, more credibility, more investors who understand the story. Leus added a shareholder-stability dimension: without analysts setting expectations and maintaining coverage, institutional and retail holders have no anchor when volatility hits. "All of a sudden your stock price drops and you're like, what just happened," said David Walker, president of Intergalactic, a St. George-based aerospace thermal management company. "You didn't have a good stable base."

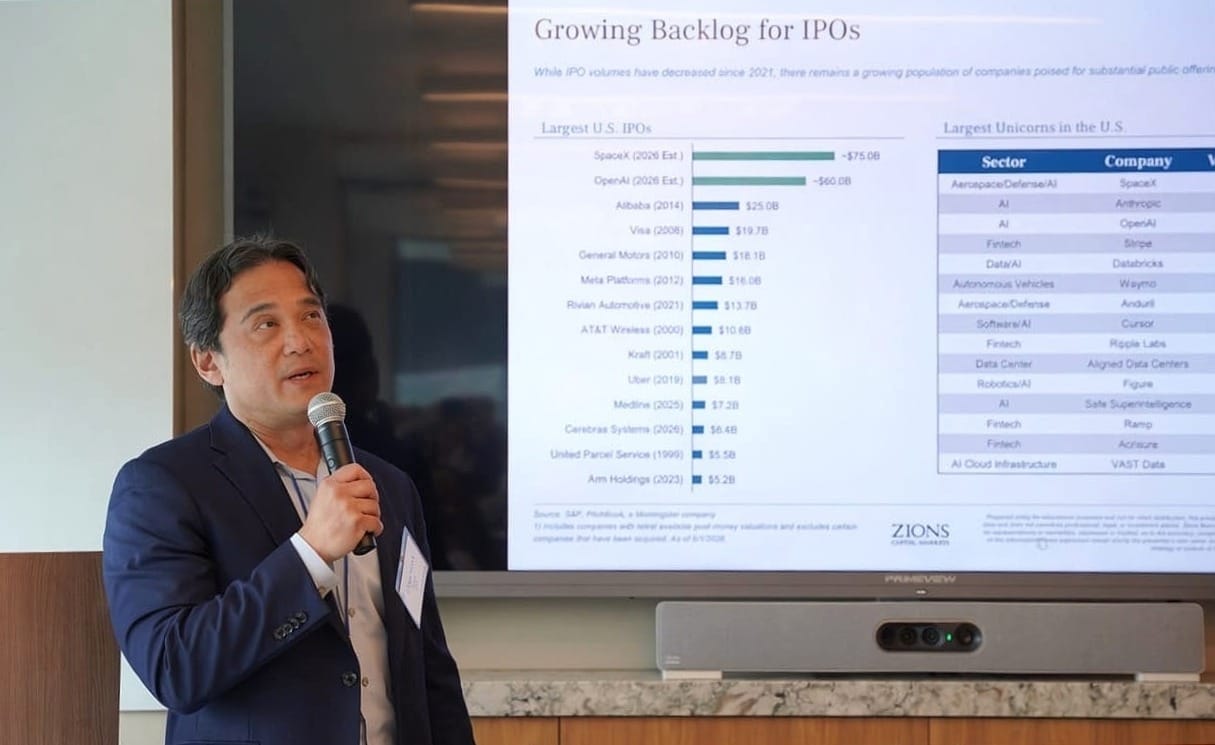

A contrarian note came from Chad Iverson, CFO of LoanPro, who listed several Utah IPOs — Domo, Pluralsight, Purple, Weave, Traeger — whose post-IPO market caps now trade well below their offering prices. The Zions data put Utah's IPO activity in stark relief: the state had nine IPOs in 2021, zero in 2022 and 2023, three in 2024, two in 2025, and none yet in 2026. Technology and healthcare together account for roughly 77% of historical Utah IPOs by sector. The median revenue for a Utah company in the year it went public was $535 million, a bar that screens out most of the state's growth-stage companies.

Utah does have a unicorn pipeline. Zions identified eight privately-held Utah companies valued at $1 billion or more: Entrata at $4.3 billion, Filevine, Podium, and Lucid Software each at $3 billion, iFit at $3 billion, MX at $1.9 billion, Route at $1.4 billion, and TaxBit at $1.3 billion. One of those — Entrata, the Lehi-based property management software company — may not stay private much longer.

David Politis, founder of Utah Money Watch, reported recently that the company filed confidentially with the SEC in December 2025 and is widely expected to price before July 4, or else wait until after Labor Day. At its last private valuation of $4.3 billion, it would be Utah's most significant IPO in years. Whether any of the others choose the public path — or whether acquirers or private equity firms get there first — is precisely the question the roundtable was convened to address.

"I wonder if it's really the right thing for the state," Iverson said of underperforming IPOs. "How can we make them better so we don't have more Pluralsights?"

Politis was direct in response: many of those companies, in his view, suffer from weak investor relations and insufficient Wall Street following — not from a structural flaw in the IPO path itself. "Their PR sucks, their investor relations is terrible. If you do a good job of telling your story, the market cap should stay up." He added that some companies simply should not go public, regardless of community enthusiasm.

Commissioner Peirce: Reducing the Burden, Restoring Focus

SEC Commissioner Hester Peirce joined the Roundtable via Zoom, offering a disclaimer that her views are her own and not necessarily those of the full commission. What followed was a wide-ranging discussion of what the SEC has proposed, what it is still considering, and where she believes the current regulatory framework has drifted from its core purpose.

Peirce opened by affirming the roundtable's premise. "I think it's very important for us to focus on this question. Having more companies in our public markets — where retail investors get access to growth, where there's better transparency, where companies can provide liquidity to shareholders and employees — there are a lot of good reasons to be public."

She outlined several recent SEC actions:

Shareholder arbitration. The commission has signaled it will not block companies that want to include mandatory arbitration clauses for shareholder disputes in their registration documents, a direct response to litigation risk cited by companies as a major deterrent to going public.

Semi-annual reporting option. The SEC has proposed giving companies the option to report semi-annually rather than quarterly. Peirce acknowledged mixed early comments on the proposal, but said she's particularly interested in whether even companies that stick with quarterly reporting might benefit from a more streamlined filing format. "Could we do anything to streamline those quarterlies so they're not as burdensome? I'm hoping we'll get some good comment on that."

Registered offering reform. A May 19 proposal would make technical but meaningful changes to the criteria for shelf registration eligibility and streamline how companies conduct follow-on offerings after their IPO.

Emerging growth company categories. A parallel proposal aims to simplify the patchwork of issuer categories — emerging growth company, smaller reporting company, and others — that Peirce described as "a nightmare" to navigate. "We've tried to streamline the categories so it's more predictable which one you'll be in."

Climate disclosure rescission. The commission has proposed pulling back its climate disclosure rule, which Peirce said was driven by stakeholder interests not aligned with long-term financial value for investors. "We really lost our focus on materiality," she said, describing the broader disclosure reform effort as a return to what Congress actually directed the SEC to do.

Research analyst restrictions removed. Peirce noted the commission had already ended restrictions on research analysts that stemmed from a previous enforcement action, a direct response to the analyst coverage problem raised repeatedly throughout the roundtable. "Lack of research analyst coverage is a reason companies don't go public, don't get coverage, liquidity isn't as good."

Where the SEC Can Go Only So Far

Participants pressed Peirce on whether these changes would be sufficient to move the needle.

For example, David Marx asked whether the SEC had studied the cumulative effect of its proposed reforms on IPO volume. Peirce acknowledged that while the commission's economists analyze individual rulemakings, no single comprehensive study of IPO deterrents exists. "Some of it is really hard to predict, but I think the combination of all these things should make it more attractive."

William Clayton, a BYU Law professor who has written on private market access and retail investors, raised a structural challenge: a 2011 study by Jay Ritter found that an important driver of the decline in small company IPOs is a product-market shift — specifically, that the ability of large incumbents to quickly replicate a startup's technology makes the acquisition channel more attractive than going public. To the extent that dynamic is in play, regulatory relief alone won't solve the problem. "Reducing regulatory burdens will only go so far," Clayton said. Peirce agreed it was a real factor and said the SEC is trying to understand what it can and can't affect.

Josh Erekson, a capital markets partner at Dorsey, raised exchange-level listing standards, particularly NASDAQ's recently tightened requirements for smaller issuers, and asked whether the SEC is engaged there. Peirce said the exchanges need to ensure listed companies meet their standards, but acknowledged the balance between investor protection and accessibility is a live question.

Dr. Colton McEwan, Project & Program Manager at BioUtah, raised a market structure concern about whether smaller, newly public companies are structurally disadvantaged by automated market makers and high-frequency liquidity dynamics. Peirce said the question is larger than newly public companies — it affects all smaller issuers — but acknowledged the commission is actively reconsidering aspects of market structure and working to encourage exchanges to experiment with different trading models for smaller companies.

On proxy advisors, i.e. firms whose voting recommendations can effectively determine outcomes for many public companies, Peirce was unusually pointed. Companies frequently complain that proxy advisors drive votes based on flawed or inaccurate information, she said, and the SEC's prior attempt to regulate them was overturned in court. "If you all want to see change, there may need to be more of a legislative approach than a regulatory approach." That, she suggested, is exactly the kind of issue worth bringing to Utah's congressional delegation.

Asked by TechBuzz about unintended consequences of the current reform push, Peirce offered a pointed example drawn from the SEC’s 2023 cybersecurity disclosure rule. The rule was motivated by a reasonable goal — ensuring investors receive timely notice of material cybersecurity incidents — but its specific requirements created an unintended problem. “If companies are being asked to report on the cyber event while they're in the middle of that event, it could be a really nice road map for the hacker who's attacking the company,” she said.

Peirce has elaborated on this concern in greater detail in her prior public statements. In her July 2023 dissenting statement on the rule, she warned that the Form 8-K incident disclosure requirement (and subsequent amendments) could provide attackers with ongoing updates about the company’s knowledge of the breach, its response progress, and potential financial impacts. She also highlighted risks from governance and strategy disclosures, which could hand cyber criminals “a roadmap on which companies to target and how to attack them.”

In her view, the cybersecurity rule illustrates what happens when regulators do not adequately account for how real-time disclosure obligations shape company behavior during an active incident. She applied this caution broadly to the current reform effort: get the balance right, or risk substituting one set of problems for another.

What Utah Can Do

Keller wrapped the roundtable with a list of state-level actions the group had surfaced. Among them: changes to Utah's corporate code and its new chancery court to make the state a more attractive home for public companies; hosting IPO runway and capital markets events to connect Utah issuers with investors; working with financial institutions to recruit equity analysts focused on Utah companies; opening discussions with the proposed Texas Stock Exchange (TXSE) — expected to launch by year-end — to facilitate listing by Utah companies; and continuing dialogue with the state's congressional delegation on securities law reform. Leus noted that Texas has made deliberate investments in becoming an IPO-friendly state, and that other states are watching. "That's probably one of the reasons why we're all here," he said.

Lance Soffe, Director of Targeted Industries at the Governor's Office of Economic Development, framed the recruitment angle: Utah is competing for companies that are already considering or in the middle of IPOs, and the state's ability to offer a supportive ecosystem — legal, financial, cultural — is part of that pitch.

Aaron Starks, President and CEO, 47G

Aaron Starks, President and CEO of 47G, raised the harder question: does Utah have the infrastructure and culture to support founders preparing for public markets? Board governance, investor relations, financial discipline — these are skills that have to be built before the S-1 is filed. "In LA it would be very different. I don't know that we have that same attitude."

Politis was characteristically direct: "You can actually take the company public anywhere. Can it be done in Salt Lake City? Can it be done in Provo? The answer is yes."

Whether it happens in greater numbers depends on the convergence of regulatory relief, cultural shift, and the kinds of sustained institutional support this roundtable was designed to catalyze. Commissioner Peirce's parting word to the group: send comments to the SEC. "We take those public comments seriously. We're dealing with a very precious resource, which is the U.S. capital markets."

TechBuzz News co-hosted the roundtable with Dorsey & Whitney, LLC. The event was held at Dorsey's downtown Salt Lake City offices.

Share this article

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.